🌍 Introduction

Global Market Crash: Late in the first half of 2025, the United States abruptly increased the rates on broad baskets of imports to effectively 50%, tugging at a string that detonated through global finance like a row of underwater explosions. Stocks, credit, commodities and currencies all tumbled in a cascading fashion that commenced with portfolio de-risking and culminated in a coordinated liquidity race for dollars. India felt the whiplash: the rupee fell, yields jerked higher and export‑linked mid‑caps showed sharp gaps. But it’s about more than just a bad week on screens. If you want to understand why markets cracked this hard, you have to follow the policy logic, the supply‑chain math, and the behavioral feedback loops that turned tariff talk into a full‑blown risk‑off regime. This long‑form explainer plots the sequence from announcement to asset repricing, translates the jargon into practicable India‑centric takeaways, and lays out playbooks for businesses, investors and households as they navigate the months ahead.

Meta description: Why 2025’s tariff shock smashed markets—policy timeline, transmission to prices, India lens, sector fallout, scenarios, and resilient playbooks.

🧭 How we got here: policy beats that set up the crash

The political logic was straightforward: pressure trading partners with tariffs, onshore sensitive supply chains, and reset the global bargaining table. In reality, this sequence produced overlaps of the shocks. First there were signs of wider responsibilities — trial balloons, speeches, leaks — to prod companies to front‑load shipments. Then, an official order raised effective rates to near 50% on broad categories such as consumer durables, intermediates and some finished goods. Importers scrambled to reprice catalogs, but retailers — addicted to certain price points — resisted. Inventories ballooned, cash cycles elongated and procurement teams took a breather. Investors around the world were reading the tea leaves as a move toward fragmentation, which would mean lower growth, increased volatility in inflation and lower margins worldwide. As models rebalanced, funds trimmed risk and correlation spikes did the rest.

📉 The market dominoes: what fell first, what fell worst

- 🔻 Equities: High‑beta export hubs were first to crack. In India, textile, gems & jewellery, auto ancillaries, and specialty chemicals led declines as U.S. shelf‑space risk translated into downgrades.

- 💳 Credit spreads: High‑yield and EM spreads widened as earnings visibility dimmed. Refinancing windows narrowed; weaker issuers shelved bond plans.

- 💵 FX: A knee‑jerk dollar bid punished Asia ex‑Japan. Rupee depreciation offered some export cushion but lifted imported inflation risks.

- 🛢️ Commodities: Oil eased on growth fears, but logistics premia and insurance stayed sticky; agri inputs oscillated as shipping patterns shifted.

- 🏦 Rates: Front‑end yields climbed where central banks signaled vigilance against second‑round price effects even as growth cooled.

🧮 The transmission mechanism: from duty to damage

A 25‑point duty add‑on is not just a stacking on of prices; it feeds up through supply chains. Take a ₹100 ex‑factory widget. Add shipping, insu r a nce and port handling—call it ₹120 CIF. Retail wants margin, promos, and markdown budgets. To push duties from 25% to 50% and the shelf math can start bloating to ₹150–₹160 equivalent. In categories in which 8–12% constitutes a good net margin during normal times, that wedge blows the feasibility up, unless someone — the exporter, the importer, the consumer — swallows pain. And when everyone singlespreads the parcel, volume goes away first — and price follows. Markets, gazing at collapsing operating leverage, mark down everything that is exposed.

📊 🧩 Comparison — three shock channels that cracked the tape

| ⚙️ Channel | 🎯 What it hits | 🔍 Why it mattered for 2025 |

|---|---|---|

| Price‑point compression | Retail pegs ($9.99, $19.99) | Broke the consumer psychology loop; retailers resisted MSRP changes |

| Working‑capital strain | Inventory turns, supplier cash | Delayed re‑orders; cascaded into factory under‑utilization |

| Geopolitical repricing | Valuation multiples | Higher long‑term discount rates for globally exposed firms |

🇮🇳 India lens: where the blow landed—and where it didn’t

For India, the jolt is uneven. Export heavy midcaps linked to US took first set of heat: Tiruppur knits, Surat diamonds, Kakinada seafood, Rajkot castings, and Vapi/Ankleshwar intermediates. IT‑BPM experienced second‑order risk, as U.S. clients postponed discretionary projects, although annuity work remained. Banks with strong retail books, limited offshore exposure and low market to market in bond portfolios were relative havens. The drop in the rupee eased invoices for a few quarters but raised the cost of imported inputs for chemicals and electronics. Smart treasury desks had opportunistically locked forwards, but weaker exporters had chased unprofitable volume, a mistake markets had punished sharply.

🧰 What investors can do now: a pragmatic playbook

- 🧭 Triaging exposure: Map portfolio revenue by U.S. share and label companies by pricing power. Avoid businesses that only win via price without brand or IP moats.

- 🧮 Balance‑sheet resilience: Prefer low net debt, liquid inventories, and diversified buyers. Watch DSO creep.

- 🧱 Hedge discipline: Layer FX forwards; avoid binary bets. Use protective puts during event windows; finance via covered calls on rallies.

- 🌍 Diversification: Rotate marginal risk to domestic cyclicals that benefit from import substitution and to EU/GCC‑exposed exporters.

- 🧑💻 Earnings revision watch: Monitor consensus cuts; add on capitulation in companies with proven design‑in positions.

Macro re‑wiring: Global Realignment—Tariff Wars Fuel Decoupling of Financial Systems

🧠 Why the sell‑off became a crash: behavior, not just balance sheets

Markets crash when everyone tries to rush for the same door at once. In 2025, three behaviors overlapped. For starters, quant funds fell over momentum and volatility cliffs, auto‑deleveraging into only-thin-enough books. Second, retail flow chased headlines selling export names and piled into perceived havens, magnifying factor swings. Third, corporate treasuries stopped ordering to preserve cash, amplifying the order‑book vacuum that equity analysts projected. This reflex loop — models → behavior → fundamentals → models — collapsed weeks’ worth of repricing into days. Volatility begats volatility; liquidity costs explode; correlations go to one.

🌐 Contagion across regions: who absorbed what

The pain reverberated along trade and financing arteries. Mexico and Vietnam were first beneficiaries of buyer hedging, but price‑point traps emerged when U.S. retailers remained unable to move MSRP. EU exporters benefited at least as much from REACH‑compliance and the energy overhang; their luxury names kept up on brand pricing. Jewellery and seafood flows continued to be channelled through the GCC although with increased price sensitivity. Japan/ASEAN did have some space in auto parts and specialized fabrics, although it took time for scale to develop, in part because of certification times. For parts and fabric, Africa/ LatAm provided post-factory product demand, if not margins.

📊 🌎 Comparison — regional ripples and near‑term outlook

| 🌍 Region | ⚡ Immediate impact | 🔭 6–12 month outlook |

|---|---|---|

| EU | Export hesitation, energy‑cost drag | Stabilization via green‑spec demand; luxury resilience |

| GCC | Jewellery/seafood inflow at keener prices | Price‑led volumes; FX stability helps retail turn |

| Japan/ASEAN | Wins in auto parts & fabrics | Slow but sticky gains after certifications |

🧩 Sectors under the microscope

- 🧵 Textiles & apparel: Retail peg rigidity punishes basics; winners pivot to functional fabrics, digital prints, and micro‑drops; losers drown in markdowns.

- 💎 Gems & jewellery: Lab‑grown offsets part of natural; story‑led independents stay sticky; mass market softens.

- 🦐 Seafood: Value‑added packs (marinated, breaded) and channel shifts to EU/GCC keep plants warm.

- ⚙️ Auto components: Guard design‑in positions; expand aftermarket in LatAm/Africa while co‑engineering cost with Tier‑1s.

- 🧪 Specialty chemicals: Stickiness comes from formulation support, alternate grades, and documentation that deters substitution.

India‑specific sector lens: India Hurts—Sectors Under Pressure as U.S. Doubles Tariffs

🧪 Case stories: four snapshots that explain the tape

One day, U.S. POs (purchase orders) tumbled 30% for a Tiruppur knitwear exporter. The team reconstructed tees in lighter GSM cotton‑poly, introduced three‑pack bundles, and pitched Germany and UAE with eco labels; margins were back to normal by quarter two. In Sūrat, a diamant house changed to a lab‑grown capsule line then restarted over to the U.S. by means of a duty‑free returning hub; QC people (mostly squeeze and polish women) got retrained. A Kakinada seafood plant co‑developed weekday menus for U.S. chains and rerouted breaded one‑pound packs of marinated shrimp to EU/GCC, which pinched farm exits. A casting house in Rajkot saved its design‑in through co‑funding PV with a U.S. Tier‑1, and at the same time increased its aftermarket SKUs in Latin America to shore up cash flow. In every picture, the image is the same: spec agility, market diversification, and process discipline trump raw discounting.

🧯 Policy responses that matter—and those that don’t

- 🧪 Targeted carve‑outs by HS line have real bite, especially where domestic U.S. consumers face visible price spikes.

- 🧳 Market access missions with pre‑booked buyer meets in EU/Japan/GCC accelerate redirection of volumes.

- 🧰 Quality & compliance grants (REACH, traceability, effluent upgrades) beat blanket subsidies; they unlock higher‑value demand.

- 🧾 Contract sanctity: pushing predictable dispute resolution and paperless customs corridors limiting dwell time helps more than rhetoric.

- ❌ Across‑the‑board rebates without productivity ties often backfire, delaying adaptation.

Legal angle: Could ‘Liberation Day’ Tariffs Be Declared Unconstitutional?

🔮 Scenario planning: three paths for the next 12 months

Keep an eye out for a quick revival of shelved SKUs if tariffs subside through carve-outs or quotas; exporters should maintain shelf-ready cartons and compliance files. For a status quo regime, expect shorter order cycles, rolling POs and bloody battles for promo weeks. If there is escalation into the adjoining HS lines, it’s about cash preservation, and contract triggers become more important than top‑line. And in all three, the edge goes to teams that can toggle between value and premium specs without sacrificing brand equity.

❓ Common questions, answered briefly

- 🙋 Will a weaker rupee fix the earnings hole? It cushions invoices temporarily but cannot plug a 25‑point duty wedge. Use the cushion for automation and EU/Japan entry costs.

- 🙋 Will U.S. buyers share the duty burden? For must‑carry SKUs, some will via spec changes and bundles. For commodity basics, expect shared pain.

- 🙋 Can India simply redirect to the EU? Not overnight. Compliance and spec differences mean a 2–4 quarter ramp, but green credentials help.

- 🙋 Is IT‑BPM safe? Mostly, but discretionary projects may get paused; outcome‑based pricing and automation protect margins.

🔎 Data to watch every week

Keep an eye on retail peg adherence in the U.S. (are $9.99s moving?), inventory turns at major chains, container rates on key lanes, credit spreads for EM, and India’s DSO trends in export clusters. If pegs break and inventory clears, the worst may be done; if pegs hold but volumes drop, brace for a longer grind.

🧰 What businesses in India should do this quarter

Re‑cost SKUs into duty‑paid vs duty‑neutral options; drop long tails. Build design pods to pitch curated micro‑drops. Lock FX opportunistically, not heroically. Negotiate rolling POs with spec flexibility and promotion‑week alignment. Invest in traceability and REACH compliance to open EU/Japan gates. Above all, guard first‑pass yield—returns nuke margins faster than any tariff.

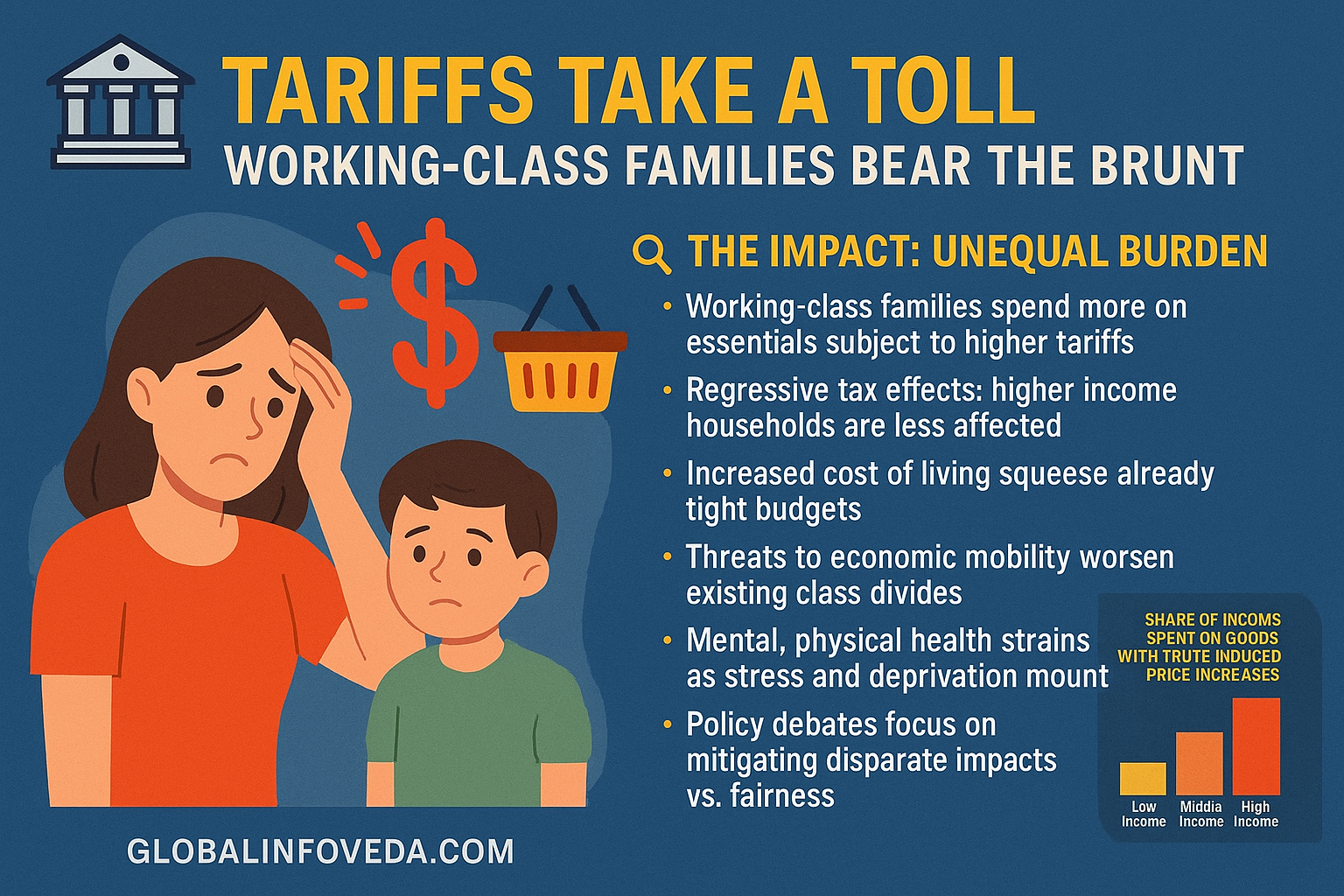

🧺 Household checklists for turbulent months

- 🧾 Budget hygiene: Recast monthly spends for food, fuel, and EMIs; assume imported inflation can pop up with a lag.

- 💳 Debt discipline: Avoid floating‑rate credit unless income visibility is strong; prepay high‑APR balances first.

- 🥫 Smart stocking: Build modest buffers for essentials if logistics stay volatile; avoid panic buying.

- 💼 Savings ladder: Keep 3–6 months of expenses liquid; step‑ladder FDs to manage rate risk.

- 🪙 Gold & hedges: Treat gold as a volatility balancer, not a get‑rich trade; stagger entries.

Independent estimates suggest the burden distribution skews toward lower‑income households when essentials face imported‑input pressure; planning buffers and pacing big‑ticket purchases can soften the hit while price signals settle.

🎯 Traders’ corner: how to avoid getting steamrolled

Trade less, size lower, hedge more. The volatility following policy shocks is path‑dependent; the first bounce can be the most difficult to short, and the first crack the most difficult to buy. Anchor to levels, but allow options to express views; go max pain up front. Keep an eye on liquidity pockets at key expiries, don’t let a headline establish your risk more than your plan. More important: Recall that correlations go to one in panics — diversification within equities doesn’t work; cross‑asset hedges and cash are your friends.

🧠 Myth vs fact

- ❌ “Tariffs just reshuffle supply chains; markets overreacted.”

✅ The financing and inventory cycles amplify the shock; working capital and retail pegs are hard constraints. - ❌ “A dollar squeeze helps exporters enough to offset duties.”

✅ A weaker rupee cushions invoices but raises input costs and servicing costs on foreign liabilities. - ❌ “We can wait it out without spec changes.”

✅ Spec agility—two approved specs per SKU—keeps shelf space and brand perception intact.

📊 💼 Comparison — assets, expected behavior, and simple hedges

| 🪙 Asset | 📈 What to expect | 🛡️ Simple hedge note |

|---|---|---|

| Export‑heavy mid‑caps | Earnings resets; multiple compression | Scale via options; add after guidance clarity |

| Banks | Better relative if retail‑heavy; MTM risk on bonds | Watch duration; use barbell deposits |

| Gold | Volatility balancer during risk‑off | Stagger purchases; avoid leverage |

🧭 Timeline—from rumor to rout

In the weeks leading up to the official elevation of duties, policy signals proliferated: off‑hand comments in interviews, talking points at conferences, and background briefings that the financial press parsed line-by-line. Procurement teams responded by front‑loading orders, shoving more containers into already cramped lanes. So, too, the ports jammed up, insurance premia skyrocketed, and in‑transit inventory expanded. When the order eventually did come in, retailers refused to break psychological price points on store shelves, so all of a sudden procurement stopped in all categories at the same time. With buyers keeping their hands in their pockets, factories that already had orders on their books encountered a deafening silence. Analysts, seeing inventory days and forward guidance crumble, punched numbers through coverage models and cut ratings. Quant strategies that had become attuned to volatility spikes and momentum breaks automatically cut positions. The interplay of policy signal, corporate reaction and portfolio mechanics compressed months of adjustment into only days, transforming an arguable policy experiment into a synchronized risk‑off shock. The takeaway is that in tightly coupled systems, even foreseeable shocks ignite outsize outcomes when they crash into inflexible retail pegs and end‑of‑quarter financial optics.

🧩 Microstructure—why liquidity disappeared in minutes

- 🧮 Quote thinning: Market‑makers widened bid‑ask as implied volatility surged, making it costly to trade size and inviting further gaps.

- 🧯 Dealer risk caps: Internal VAR limits cut principal activity; inventories were reduced precisely when clients needed exits.

- ⚡ Gamma effects: Short‑dated options positioning forced delta hedging, turning small price moves into chasing flows.

- 🧊 ETF plumbing: Basket imbalances meant some ETFs traded at discounts/premia to NAV, amplifying the optics of panic.

- 🧱 Collat calls: As prices fell, margin and collateral calls hit simultaneously across desks, pulling more sellers to market.

- 🕳️ Dark to lit migration: Liquidity moved from dark pools to lit venues as urgency rose, making screens look worse and accelerating copycat behavior.

🧠 RBI & Government matrix—what stabilizes without masking price signals

India’s policy toolkit is effective when it maintains price discovery while buffering against the worst cash‑flow shocks. RBI can draw upon FX liquidity windows and fine‑tune durable liquidity to avoid disorderly rupee moves without needing to defend any magic number. Rates policy should stay data‑dependent, balancing the inflation pull from abroad vs. ground wobble. On the fiscal side, targeted interest subvention linked to productivity (testing labs, REACH upgrades, energy efficiency) is better than the siren call of blanket rebates. Customs facilitation — paperless corridors, gates open longer, faster adjudication — brings relief faster than the sabre-rattling we’ve heard. Clean cluster dashboards for textiles, gems, seafood and components can help states deploy creches, transport and safety nets that keep women workers and skilled migrants through the downcycle. ‘Crystal clear’However, above all policy communication should be crisp: explain the objective, what metrics are being watched and at what point any intervention is going to sunset in order to avoid moral hazard.

🧰 CFO survival kit—keeping factories warm and lenders calm

- 🧾 Re‑cost every SKU under two lanes: duty‑paid to U.S. vs redirected to EU/GCC/Japan/ASEAN; shelve long‑tail items that destroy working capital.

- 🔄 Rolling POs with buyers: trade spec flexibility and promotion‑week alignment for volume visibility.

- 🧱 Cash firewall: ring‑fence 90–120 days of payroll and utilities; index discretionary spends to order backlog.

- 📊 Bank dashboards: share weekly DSO, first‑pass yield, and order books; invite lenders to floor walks to build trust.

- 🌐 Compliance leapfrogs: pull forward traceability, AEO documentation, and sustainability metrics to win EU/Japan bids.

- 🛠️ Throughput hacks: SMED in sewing/finishing, carton redesign, milk‑run trucking; small operational wins defend margin.

📈 SIP & retail investor guide—protecting small money from big shocks

Long‑horizon savers in India should bear in mind that calendar crashes are part of equity math but sequence risk matters. Keep SIPs running — you can’t time your luck to perfection — and diversify across quality factor funds and short‑duration debt to soften the blows. Don’t jump on export‑only stories in the first downdraft; wait for earnings revisions to land. India‑domestic beneficiaries of import substitution on one hand of the barbell, and global-quality franchises with substantial pricing power on the other. Now is the time to be holding a bunch of gold or gold ETFs as an insurance policy against volatility and not for anything else and to avoid ending up in a house of leverage masquerading as sophistication. Most importantly, write out your max drawdown comfort and simply follow it, systems outdo gut when headlines are screaming.

🧪 Supply‑chain redesign—how exporters can buy time and defend shelves

- 🧭 Dual finishing: perform core processes in India, shift final finishing/pack to a duty‑neutral hub to retain partial U.S. volumes.

- 🧪 Spec agility: maintain value/premium spec pairs per SKU; let buyers keep pegs without killing brand equity.

- 🧳 Market mix: warm up EU and Japan with pre‑booked audits and language assets (catalogs, care labels).

- 📦 Carton science: reduce volumetric weight; pair with shared freight across cluster peers.

- 🧰 Content & story: for independents, sell craft, origin, and sustainability to earn assortments that pay for quality.

🛢️ Commodities lens—energy, metals, and agri under a tariff regime

Normally energy will fade on growth anxiety, but 2025 offered a twist: you could even see the shipping risk premia and insurance holding up as crude slackened off. That meant the dynamics of diesel and bunker‑fuel cut back some of the relief for logistics‑heavy exporters. In metals, tariff talk whacked aluminium and steel proxies on assumed slower construction and appliances, though the restocking phase can allow for some violent bear‑market rallies — dangerous to short late. For agri, fertilizer inputs and feed costs gyrated with freight, biting at shrimp and processed food margins. Smart procurement teams layered time‑spreads and diversified origin to smooth the bumps, treating commodities not as a gamble but a series of budget guard‑rails.

🧰 Hedging cookbook for MSMEs—simple, repeatable, audited

- 💱 FX micro‑layers: book small forwards weekly (10–15% of exposure) to avoid big directional mistakes; publish a hedge policy your board signs.

- 🧾 Receivable discounting: diversify across platforms so one lender’s appetite doesn’t freeze your entire book.

- 🛡️ Selective credit insurance: cover the top 20 counterparties; use premium savings to fund QC upgrades.

- 📉 Options for event risk: buy protective puts around policy dates; finance them by writing small covered calls against surplus inventory hedges.

- 🧪 Natural hedges: source a slice of inputs in USD where possible so revenue and cost move together.

🧪 Case story—Panipat home‑textiles holds share in Europe

A home‑textiles unit in Panipat got a 40 percent U.S. whack. The team steered woven throws and bath sets towards Germany and Scandinavia following a quick REACH alignment and sustainability audit. They relied on digital prints for smaller curated drops and, in some cases, teamed up with two cluster peers for shared freight and VMI pilots with a discount chain. Both capacity utilization rose above 82% within two quarters, and EU share increased from 22% to 43% by maintaining women stitchers on payroll.

🧪 Case story—Moradabad metalware survives on design and drops

A brassware exporter from Moradabad lost big‑box orders but pitched story‑led collections to independent boutiques in the U.S. Northeast and EU. By building a design pod and hiring a part‑time stylist for photo assets, the firm sold limited‑run candle stands and serveware at higher ASPs. Gross margin improved even on lower volume; the firm secured a store‑in‑store trial with a European home chain for the festive quarter.

🔎 Glossary—jargon that crowded the headlines, translated

- 🧾 MSRP/peg: the shelf price that anchors consumer behavior; breaking it hurts sell‑through.

- 🧮 First‑pass yield: share of output that passes QC without rework; a quiet margin lever.

- 🧳 AEO: Authorized Economic Operator; certification that speeds customs in partner countries.

- 🧫 REACH: EU chemicals regulation; compliance unlocks access for textiles, leather, chemicals.

- 🧰 SMED: quick‑changeover method that raises throughput without capex.

- 🧱 VAR/gamma: risk and option‑sensitivity metrics that force dealers to cut or add exposure quickly.

❓ More questions we kept hearing—clear answers

- 🙋 Will across‑the‑board rebates help exporters? Only when tied to productivity milestones; untargeted rebates delay adaptation and waste scarce fiscal space.

- 🙋 Should MSMEs chase any buyer who calls? No. Filter by payment terms, brand reliability, and historical return rates; bad accounts nuke cash.

- 🙋 Are warehouse clubs a safe haven? They can be, because members accept bundle packs and occasional peg moves; but they demand ruthless on‑time, in‑full.

- 🙋 Do independents matter? Yes—story‑led independents keep value perception alive and accept smaller drops, giving factories schedule stability.

- 🙋 Can co‑manufacturing abroad fix everything? It helps margins and access, but you must protect process control and IP; keep the crown jewels in India.

🧮 Stress‑test template for CFOs—three quick ratios

Indian exporters can sanity‑check with a basic dashboard for resilience. Directionally, we suggest three key figures as of the time you take out a loan: Coverage ratio: months of payroll + utilities you can fund from cash/undrawn lines at current run‑rate; target 3–4 months. In the second, trend-line tone from the first‑pass after spec downgrades — quality slippage produces returns that decimate delicate margins. Third was the DSO delta: how stretched are days receivables following the renegotiated terms; anything north of +10 days requires a financing solution. Put these together with a rolling 13‑week cash flow, and you’ll spot trouble early.

🧠 India’s regional exposure—state‑level nuances that shape outcomes

Tamil Nadu and Punjab suffer apparel shock early due to their knit clusters and high optimisation of women; targeted creches and safe transport can only help retention. Surat and Vadodara in Gujarat counter gems/chemicals with a hefty engineering base that can backfill some wage loss. The growers of Andhra Pradesh, and of the East Coast, see immediate ripples in the seafood market; cold‑chain dependability and farm credit terms determine how many ponds go fallow. Moradabad and Kanpur in Uttar Pradesh depend on design and compliances to retain EU share.” And what separates a short shock from a long scar varies state by state, though it is often a combination of cluster services, testing labs and buyer roadshows that keep the conversation going even if the orders are thin.

🧠 What to watch in corporate results—tell‑tale footnotes

Seek out inventory write-downs, return provisions and contract liabilities that are red flags that lines have been canceled. Parse your commentary on weeks promoting and bundle acceptance — is space being created by retailers or terms being squeezed? Second-guess capex deferrals vs small, high ROI automation that maintains good throughput. “Look at how many SKUs even have dual specs approved; that single data point is predictive of shelf survival much better than blanket cost‑cut talk.” Lastly, follow the EU/Japan customer ads, these markets will pay up for traceability and testing long after the volatility is gone.

🧠 City‑level resilience—finance, ports, and talent

For speed, Mumbai and Gujarat ports count; days matter, and extended gate hours, and the availability of containers can shave many of these away. Bengaluru and Hyderabad talent pools also assist exporters in building pods specialized in data, design, and automation without the need to move factories. The Delhi‑NCR serves as a base for the buyer meets, and policy discourse enclaves; cluster associations that have live dashboards of orders and hours, are being fawned targeted relief. The cities that emerge stronger are those that turn this shock into a sprint on compliance, design and digital tooling.

📚 Sources

- Reserve Bank of India (RBI) — Bulletins on external sector and market developments: https://www.rbi.org.in/

- World Trade Organization (WTO) — Trade policy monitoring and statistics: https://www.wto.org/

- U.S. Trade Representative (USTR) — Tariff announcements and country notes: https://ustr.gov/

- Congressional Budget Office (CBO) — Analyses of tariff effects on prices/incomes: https://www.cbo.gov/

🌟 Final Insights

The crash of 2025 did not happen in a mistery: It was a clear chain reaction- frorn policy shock to retail peg breaks, from working capital stress to valuation compression, from behavioral reflexes to forced deleveraging. India’s advantage, as ever, is adaptability: clusters that re‑engineer specs, companies that defend design‑in positions, households that keep debt clean, and investors who respect liquidity while keeping an eye open for quality at fair value. The next wave will reward discipline over drama — less chasing headlines, more building moats in compliance, traceability and customer repeatability.

👉 Explore more insights at GlobalInfoVeda.com

{kind=link}