🌏 Introduction

Why did the US declare a 25% “new” tariff for India-origin goods in 2025 — and why did the actual rates rise to nearly 50% for a variety of HS lines? The answer mixes trade deficits, reciprocity politics, Russia-related sanctions, and a calculation that pressuring American retailers and households on price is an acceptable expense for strategic leverage. The move will reshape export math, cluster employment, and supply‑chain routing — at a minimum India will make the long‑overdue pivot to design‑led value, compliance excellence and multi‑market resilience. This explainer follows the policy chain, unpacks legal authorities, checks stated motivations against reality, and turns all of that into in‑factory actions that maintain orders.

Meta description: The U.S. 25% tariff on India‑origin exports mixes trade, Russia‑energy pressure, and reciprocity. See motives, legal basis, sector impact, and practical playbooks.

🧭 The policy chain that led to August 2025

The 2025 round began with Washington renewing a policy of reciprocal tariffs as a means of narrowing perceived imbalances and punishing what it portrayed as unfair barriers overseas. In the spring, two disparate tracks converged: a sweeping reciprocity order under IEEPA, and a constriction of the national‑security rationales of Section 232, through a new oil‑linked penalty against buyers of Russian crude. Following a brief interlude that gave way to somewhat depressed headline rates, the extra 25% on India transitioned from draft to enforcement in early August, as customs guidance appeared in mid‑month and port operations adjusted codes shortly thereafter. In the U.S., retail calendars adjusted overnight; Indian exporters grappled with re‑opened contracts, duty‑sharing talks and rush requests for re‑designing SKU.

⚙️ Legal levers used by Washington

- ⚖️ IEEPA authority: frames economic penalties as tools to address national emergencies, including Russia‑related conduct; enables additional ad‑valorem duty layers.

- 🛡️ Section 232: ties certain tariff actions to national security, widening the scope of products that can be covered without new legislation.

- 🧾 Presidential proclamations & EOs: modify HTS chapters and direct CBP on administration, carve‑outs, and transition windows.

- 🧭 USTR coordination: aligns with ongoing market‑access disputes; synchronises messaging on reciprocity and compliance.

🧪 Motives behind the move—trade, energy, geopolitics

The declared objectives were threefold. One, to bring down a bilateral goods deficit that the White House depicted as proof of unequal access. Second, to continue punishing what are seen as strategic Russian oil purchases by the Americans by imposing an extra duty on a big, high profile buyer. Third, to force India to negotiate on long‑stalled market‑access asks in dairy, e‑commerce, data and standards, on the theory that price pain would bring about concessions. Each charge has some validity, and each one also has counter‑arguments — especially when it comes to consumer prices in the U.S., potential supply shock threats and the optics of punishing an Asian‑Pacific ally while making nice with China on other files.

📊 Motive–evidence–counterpoint

| Motive | Evidence cited | Counterpoint |

|---|---|---|

| Reciprocity | Tariff/NTB gap vs India | WTO‑bound rates and ongoing reforms narrow gaps already |

| Russia pressure | High share of Russian crude in India’s import basket | Energy security + price stability during global shocks |

| Consumer relief | Claim that tariffs force supplier price cuts | Studies show pass‑through → higher household costs |

🧩 How 25% became ~50% on many lines

Its 25% add‑on stacked on top of layers that came before. For a few of the HTS chapters, the cumulative rate jumped to ~50% when previous actions, CVD duties, or preferences were eliminated from the rates. For apparel, a nominal 25% compounded on current duties could wipe out the narrow CMT margin unless suppliers and buyers can spread the pain through spec trims, pack‑downs, and/or shifts in delivery date. In jewellery, where promotional events reinforce sticker psychology, even a 10‑point move can take down a season—unless retailers adjust to lab‑grown blends and ESG storytelling that’s friendly to small premiums. The math is unforgiving, but not without hope if factories start with engineering‑for‑affordability, not blind discounting.

🧾 Exemptions and grey areas to watch

- ✅ Pharmaceuticals/APIs: widely referenced as exempt, but watch intermediate chemicals with indirect exposure.

- ✅ Smartphones & select electronics: carve‑outs exist; accessories remain exposed and vulnerable to re‑interpretation.

- 🔍 Ambiguous classifications: mixed‑material goods, sets, and kits invite HS disputes—seek binding rulings.

- ⏳ Transitional relief: cargo onboard before a given date may qualify—document BL and export timestamps.

🧶 Sector impacts—labour‑intensive clusters at risk

The stigma slams worst into textiles & apparel, gems & jewellery, leather, seafood and elements of auto components — exactly the ones that form the bedrock of MSME‑rich districts. One of the most pressing challenges for Tiruppur knitwear factories is to re‑cut patterns, consolidate colorways, and ship faster replenishments to save their shelf slot. Surat polishers are ricocheting between lab‑grown exposure and the defence of natural stones on the basis of grading and provenance. Andhra seafood units step up temp telemetry and value‑added formats to protect price. In both cases, the narrative I write on behalf of US merchants is reliability + evidence: less claims, on‑time windows and clarity on landed‑cost.

Impacts of Trump’s 25% India Tariff on Indian Export Sectors

🛠️ Sector mitigation plays that work

- 🔧 Duty‑inclusive ladders: present value and premium options with transparent landed math.

- 🧵 Spec trims: lower GSM, rationalise trims, merge panels; protect perceived quality.

- ⏱️ Speed to shelf: near‑port consolidation, locked sailing windows, and carton‑to‑shelf packaging.

- 🧪 Evidence packs: AQL logs, photo trails, and HTS rulings build trust and reduce port friction.

- ♻️ Certification: OEKO‑TEX, ASC/BAP, R2/ISO to unlock compliant buyers and better margins.

🗺️ Russia, energy security, and why India bought that oil

India’s refining system is designed to take advantage of spot crude purchases; in 2022–2025, Russian barrels were the cheapest reliable supply in a turbulent world. New Delhi said energy access was a development imperative and should not be seen as an endorsement of Moscow. Washington, however, saw the flows as budgetary relief for Russia, which was why the penalty layer was added to reciprocity. The friction raises a deeper question: can strategic partners disagree on design of third‑country sanctions and still cooperate on security in the Indo‑Pacific? For exporters, the specific response is largely beside the point — duty math is a fact of life, so learn to live with it.

⚖️ Lawfare and constitutional debates in the U.S.

- 🏛️ Non‑delegation murmurs: critics argue that open‑ended IEEPA/232 uses sidestep Congress.

- 📜 Judicial review: courts often defer on national security; litigants test procedural limits instead.

- 🧭 WTO implications: reciprocity narratives strain MFN norms; disputes will be lengthy and uncertain.

- 🧯 Retailer/industry suits: some sectors may pursue injunctions or seek temporary relief via administrative channels.

Legal Battle Over Trump’s “Liberation Day” Tariffs: Constitutional Limits

📊 Where pain concentrates—quick matrix

| Sector | Exposure to U.S. | Mitigation priority |

|---|---|---|

| Apparel | High for basics | Spec trims + speed + evidence packs |

| Jewellery | High for mid‑market | Portfolio mix (lab‑grown + natural), ESG proof |

| Seafood | Medium‑High | Telemetry + value‑added formats |

🧮 A simple cost bridge

| Scenario | Landed change | Typical outcome |

|---|---|---|

| Before Aug 2025 | 0% incremental | Normal discount cycles |

| +25% add‑on | +18–25% after splits | Share pain; redesign SKUs |

| Toward ~50% | +40–55% by HS line | Cancellations or re‑sourcing unless value proven |

🧰 MSME survival kit

- 🧾 Standard re‑quote pack: landed math, duty‑share options, and three spec‑trim variants.

- 💳 Liquidity: combine PCFC with invoice discounting; weekly sweep of refunds/drawback/RoDTEP.

- 🧵 Process upgrades: fabric inspection cams, marker optimisation, and digital QC logs.

- 🤝 Cluster consortiums: pooled freight, shared testing labs, and buyer roadshows.

- 💬 Transparent comms: publish OTIF, claim %, and POS turns to earn extensions.

🧭 Negotiation scripts that earn yes

- 🗂️ Evidence first: “Attached are HTS rulings, BL dates, and AQL logs—we propose these two duty‑smart variants to keep your entry price.”

- 💡 Two ladders: “Hold the value ladder at last season’s ticket; launch a premium capsule with QR traceability to lift margins.”

- 🔁 Calendar swap: “Shift one promo; we’ll buffer inventory near port so fill‑rates hold.”

- 🧪 Pilot tranche: “Approve 10% volume on redesigned specs; if sell‑through clears 70% by week six, we roll to 100%.”

🚚 Supply‑chain levers that pay back

- 🚢 Sailing discipline: book two weeks early; avoid rollovers that kill promotions.

- 📦 Carton‑to‑shelf: reduce DC touches; win compliance scorecards.

- 🧊 Cold‑chain logs: live telemetry for seafood trims claims.

- 🧭 Alternate ports: test Mundra/Ennore vs default; dwell is the real tax.

- 🧰 UPC continuity: preserve barcodes through redesign; retailers hate resets.

🌍 Where to pivot—corridors beyond the U.S.

The tariff shock can only hasten India’s need to diversify demand. Proof that sustainability and traceability pay-off in price premiums for EU shelves. British jewellery and fashion markets love craft and rapid storytelling. UAE supplies re‑export hubs; Japan/Korea value consistency and paperwork. Africa and Latin America start with agri‑processing and entry‑level apparel. The strategy isn’t fleeing the U.S.; it’s creating multi‑market shock absorbers so that no one policy reversal can stop production.

How India Can Diversify After Trump Tariff Shock: ASEAN, EU, and Beyond

🧵 Two grounded examples from the shopfloor

Example 1 — Knit basics. A Tiruppur factory supplying a U.S. discounter faced a sudden 25% layer on 600,000 tees. The buyer demanded a 9% FOB cut or a redesign. The team executed a lite‑knit variant (‑10 GSM), replaced rivets with bartacks, merged colorways, and tightened markers. Savings: 5.8% of FOB. They split the remainder via a duty‑sharing addendum and added an in‑season reorder clause tied to sell‑through KPI. The line survived.

Example 2 — Diamond bands. A Mumbai studio saw U.S. partners push lab‑grown hard. The studio separated workflows: natural lines got stricter grading and provenance QR; lab‑grown moved to fast capsules for promo weeks. A small rebate linked to six‑week sell‑through protected cash flow while defending natural margins with ESG credentials.

📅 90‑day plan for commercial teams

- ⏱️ Days 0–30: freeze duty‑sharing language; file binding rulings; build an internal landed‑cost explainer; lock yarn/metal buys for 60–90 days.

- 📦 Days 31–60: pilot spec‑trim variants on 10% volume; stand up near‑port consolidation; start POS dashboards with top accounts.

- 🧭 Days 61–90: expand winning variants; test ASEAN assembly where math works; tie payment milestones to CBP clearance.

❓ FAQs that business teams are asking

- Is the new duty universally 25%? No. The 25% add‑on stacks over existing layers; many lines feel ~50%.

- Are smartphones and pharma truly exempt? Broadly yes, but check accessories, intermediates, and bundles for exposure.

- Does a weaker rupee solve it? It helps FOB competitiveness, not a 50% wall—use gains to upgrade and de‑risk.

- How should we talk to consumers? Be transparent on duty‑driven pricing and offer value via bundles or warranties.

U.S. Families Could Pay $3,800 More a Year Due to Tariffs

📈 Investor and rupee lens

Increased duties reduce order visibility, and extend working‑capital cycles. Equities sell first and model later as rupee weakness partially offsets FOB pain but signals imported inflation. Analysts will watch bank lending to export clusters, NPA drift and commercial paper spreads for mid‑caps linked to US retail. Blow some FMCG bubbles in onion pockets Onion pockets refer to dollar revenue kalonji pockets Defensive pockets are IT services (dollar revenue) and pharma (exempt lanes) The debate over household costs in America is also not insignificant: if U.S. consumers resist price hikes, retailers may ultimately be forced to stomach selective price increases, versus constantly squeezing suppliers.

Market Fallout: Trump’s Tariffs Send Rupee Weak, Shake Investor Sentiment

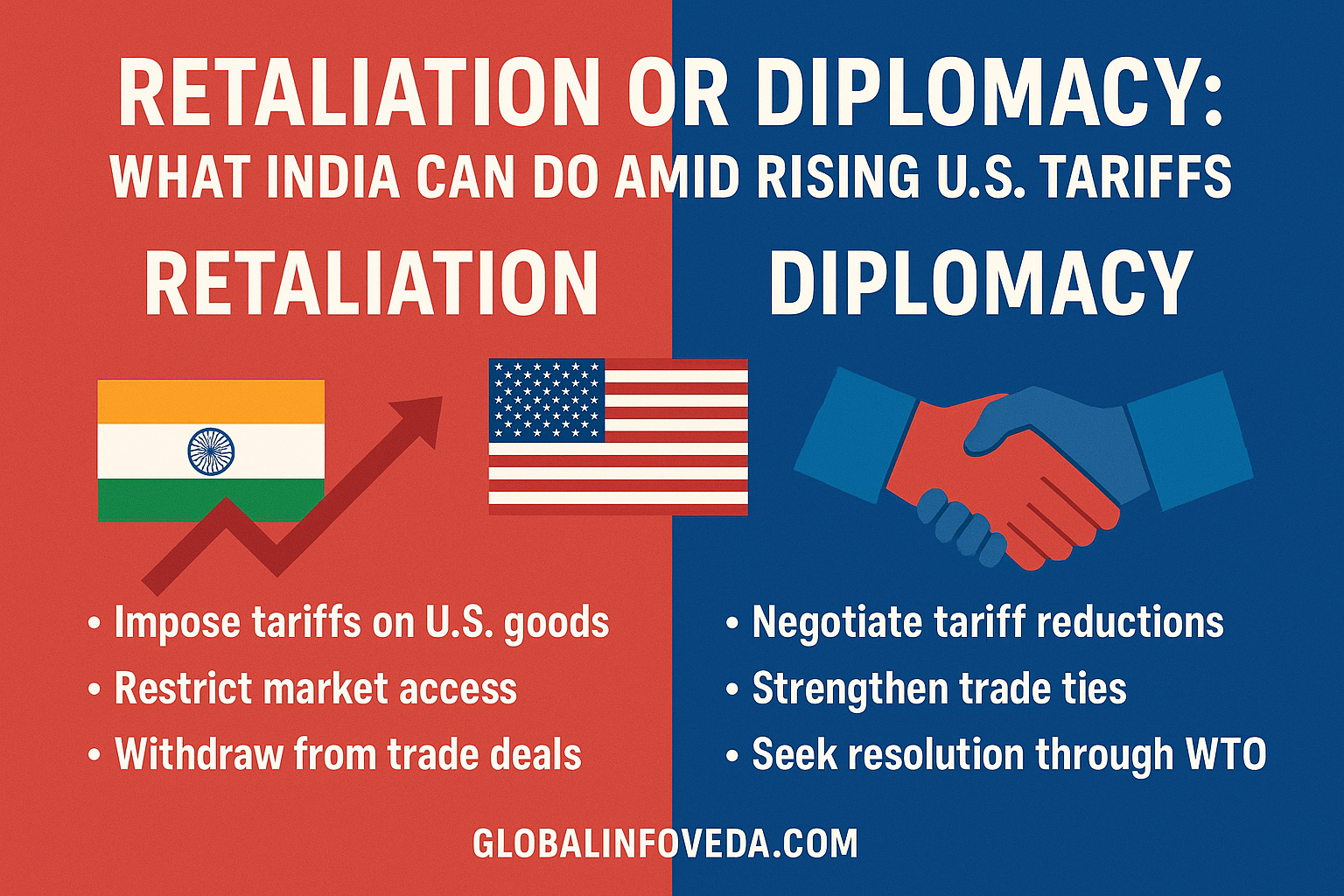

🧭 Policy asks and diplomatic off‑ramps

New Delhi can concentrate on speedier input‑GST refunds, higher-rate priority export credit and expanding the capacity of testing labs to reduce port holds. Diplomatically, narrow issue‑linked offsets (data rules, standards cooperation) might yield partial relief without breaking agriculture red lines. For Washington, metrics of success should be compliance and predictable supply, not never-ending shocks that re‑source to third countries. The duty footprint can be shrunk by technical work done quietly and without daily headlines.

🧭 Historical backdrop — from steel to smartphones

The 2025 tariff shock is also a part of a broader history of U.S. experiments with protection. Safeguards on steel in 2002 sought to protect mills but raised costs down the chain, prompting a pushback from the W.T.O. Section 232/301 duties were also weaponized by the Trump administration to rewrite the rulebook on tariffs as a tool of industrial policy and geopolitics in 2018–19. Retailers mastered the art of re‑sourcing, compressing assortments and pushing vendor finance harder. By 2025 Washington had a tested playbook: Argue national security grounds, set headline rates, sprinkle a few exemptions, and hope market pressure would bring in concessions. India’s distinction is numerical and reciprocal: it isn’t a niche supplier, but a systemic partner in pharma, IT services and a growing controller in the manufacturing internet. As a lever penalty must hence have consequences over MSME dist ricts, port logistics and household income many chapters away from an individual HS chapter.

🛒 Retailer calculus — how U.S. merchants react

- 🧮 Entry price point protection: preserve $X.99 tickets with pack‑downs and spec trims before raising stickers.

- 🔁 Origin shuffle: split volumes across ASEAN and existing India partners; avoid full resets that risk quality.

- 📅 Calendar edits: shift promotions to weeks with better ocean reliability and confirmed fill rates.

- 💬 Vendor scorecards: tie shelf space to OTIF, claim %, compliance audits, and returns.

- 💳 Extended terms: demand longer payment cycles while asking vendors to absorb duty shock.

- 🧑⚖️ Legal guardrails: insist on clean HTS files and origin evidence to reduce seizure risk at entry.

🇮🇳 Domestic policy response — what New Delhi can actually accelerate

New Delhi’s quickest levers are functional more than theatrical. Input‑GST refunds can be clocked to weekly cycles; RoDTEP rates can be clarified; testing labs near clusters can trim port holds; export credit windows can widen for firms displaying documented gains in efficiency; and logistics — from rail spines to near‑port consolidation — can be unlocked through small fixes with big velocity effects. States can provide power tariff relief and skill vouchers for shopfloor up‑skilling such as machinery maintenance that leads immediately to (higher) first‑pass yield. None of these are headline diplomacy jobs; they are raises-your-hand little murals that pay back within quarters, not years.

🧭 Reciprocity vs WTO — decoding the argument for business teams

Reciprocity may sound intuitive — the other side’s barriers are what you match — but the WTO has grounded trade in MFN (most‑favoured nation) and bound rate commitments. The U.S. argument shoots a national security needle to step outside ordinary constraints; its legality will be challenged in court, but the timeline for redress is unclear. Trade can sponsor this resilience the same way it’s helped restore multilateral trust: for exporters, this means the wall stays up until 2025–26, and move to build multi-market resilience now. Don’t frame negotiations as political battles; anchor outside asks to consumer protection, safety and predictability — issues that merchants can sell internally.

🧰 Documentation and compliance — friction you can actually remove

- 📄 Binding rulings: pre‑clear ambiguous HTS lines to lower random holds.

- 🧾 Evidence packs: time‑stamped photos, AQL logs, and dye/finish CoAs reduce disputes.

- 🏷️ Label/UPC continuity: do not force resets; barcode stability matters to retailers.

- 🔍 Lot traceability: QR trails for trims, fabrics, or stones help defend price and unlock premiums.

- 🧪 Third‑party inspection: selective pre‑shipment checks buy leverage in duty‑sharing talks.

💱 Currency and hedging — using INR wisely

A lower INR brings some short-term relief on FOB prices, but that’s not policy. Lock in a slice of benefit on deals and not on spot (and roll back into BL) and ensure forward covers are linked to shipment gates ( book on PO – roll at BL – square at outturn).” Offset by purchasing inputs in dollars to hedge with natural hedges by importing a portion of your input supply. Publish a brief FX discipline note to buyers so that they see you handling volatility professionally, rather than opportunistically.

🧪 Deeper example — seafood unit under pressure

Prices went up even beyond the reasonable retail price after the 25% layer were realised on account of a processor on the Andhra Coast exporting club ‑ size shrimp packs. The plant didn’t just make blunt cuts of course; but re‑worked the value proposition- it introduced marinated/RTC variants, added live temperature telemetry, optimized glaze to protect yield. Drew on a shared 3PL contract to open an East Coast port lane to lower dwell variance. The purchaser accepted reduced pack size with no change in shelf ticket; claims dropped 22% after temp‑excursion alerts were linked to route solutions. The plant formalized these changes in a basic buyer dashboard that now serves as the foundation for duty‑sharing extensions.

🧭 Communications playbook — what to say, when

- 🧭 Kickoff: “Here’s our landed math and three design variants to keep your entry price. Evidence pack attached.”

- 🧰 Mid‑cycle: “We hit OTIF 97% and claims fell two points; requesting 90‑day duty‑sharing extension.”

- 🧩 Exception: “Color variance above threshold; we propose in‑market rework under our right‑to‑repair clause.”

- 📈 Quarter close: “POS turns cleared target; unlocking the in‑season reorder clause preserves shelf space.”

🧭 Local relevance — how this touches Indian cities you know

- 🧵 Tiruppur: invest in open‑width processing, small‑lot dyeing, and CAD marker mastery; trim GSM smartly.

- 💎 Surat/Mumbai: build lab‑grown capacity while defending natural with provenance; tighten consignment windows.

- 🐟 Kakinada/Vizag: temperature‑logged reefers, pre‑cool protocols, and club‑pack formats.

- 🛠️ Pune/Nashik: VMI near U.S. OEMs, tighter PPAP files, and precision machining to raise switching costs.

- 🧪 Ankleshwar/Vapi: compliance stacks and REACH‑style discipline; sell stability, not just price.

🧠 More FAQs — edge cases that keep coming up

- Can the duty be rebated through creative routing? No—substantial transformation rules and U.S. documentation close obvious loops; use ASEAN assembly only when real value‑add exists.

- Will Europe follow? The EU emphasis is on sustainability and traceability; prepare for documentation, not mirror tariffs.

- What happens if duties roll back? Keep redesigned SKUs and bank margin to rebuild balance sheets; don’t rush to undo efficiency.

- How to brief workers? Translate duty into per‑piece and minutes‑saved metrics so teams see progress they control.

📚 Sources

- The White House — executive order and fact sheets clarifying additional 25% duty and carve‑outs: https://www.whitehouse.gov

- U.S. Customs and Border Protection (CBP) — operational guidance on new tariff requirements and administration: https://www.cbp.gov

- Congressional Budget Office (CBO) — estimates on tariff revenue and economic/household impacts in 2025: https://www.cbo.gov

- Reuters — reporting on the roll‑out, sector exposure, and exemptions (Aug 2025): https://www.reuters.com

🧠 Final insights

The 2025 25% tariff on India‑origin goods, compounded to ~50% in various line items, is both a lever and a litmus test. It seeks to compel concessions on market access and to impose — but not through a shooting war — Russia‑energy penalties, but it may also generate U.S. consumer inflation and the unraveling of the past two decades of strategic alignment. Indian organizations who go first—engineering SKUs for affordability, demonstrating compliance, and developing multi‑market demand—will keep their lines running, while the companies they compete against stall. Some policy fixes in Delhi and quiet technical work in Washington can lower the friction more quickly than rhetoric. What cannot wait is execution: evidence-led negotiations, quicker logistics and cash-cycle discipline.

👉 Explore more insights at GlobalInfoVeda.com

{kind=link}