🌏 Introduction

India’s export economy began 2025 with a healthy headwind of demand only to hit a brick wall of sorts with the announcement of a 25% India‑specific tariff by the United States (further piled on top of a reciprocal tariff regime that commenced in April and raised by late August indicating an effective 50% for many HS lines). Indian export sectors — from textiles and apparel and gems & jewellery to auto components, chemicals and seafood — saw the new duties immediately play carnage play with landed‑cost math, purchase orders and seasonal inventory bets. This deep‑dive breaks down what changed, who stands most exposed, and how to adjust—with sector matrices, pricing math, state‑level context, and realistic playbooks for MSMEs as well as bigger businesses.

Meta description: How a US 25% tariff rate (rising to 50% on many lines) hits Indian export sectors, with sector impact tables, case studies, cost math, and survival strategies.

🧭 What changed in 2025 — timeline and mechanics

The year began with the administration in Washington signaling response with tariffs being the way to cure trade deficits. Over the summer, orders and exemptions shifted quickly. So, in early August, the U.S. announced an additional 25% duty on India-origin goods for late August (with carve-outs — e.g., smartphones and pharmaceuticals — some transitional relief for cargo already on the water, and enforcement at customs through HTS codes). Within weeks, the SCOD (baseline duties + reciprocal + India‑specific add‑on) on numerous Indian lines effectively doubled to ~50% when layers were collated, significantly altering U.S. landed costs.

This matters for three reasons. First, the order book for fall/holiday retail was already nailed down; sudden duty hikes entail re‑negotiations or cancellations. Second, there’s spotty transfer to U.S. consumer prices —discounters squeeze suppliers before lifting shelf tags. Third, it comes in a time of rupee volatility, making hedging and EMI decisions more complex for capex-heavy exporters.

Why Trump Imposed a 25% Tariff on India: Trade, Russia, and Penalties

📦 Who is most exposed — by product family

- 🧵 Textiles & apparel: high price elasticity, thin margins, seasonal collections; quick buyer substitution to Vietnam, Bangladesh, Indonesia.

- 💎 Gems & jewellery: surge pricing meets tight credit; U.S. retailers time promotions, squeezing Surat and Mumbai polishing hubs.

- 🦐 Seafood: cold‑chain costs + duty spikes risk shrimp cancellations; FDA compliance costs cap renegotiation headroom.

- 🧪 Chemicals: mixed exposure; organic chemicals and dyes face intense competition; buyers can pivot to EU/ASEAN suppliers.

- ⚙️ Auto components & machinery: OEM contracts include escalation clauses, but model‑year deadlines constrain flexibility.

- 📱 Electronics: many HS lines exempt (for now); watch IT hardware updates and any carve‑out revisions.

- 🧴 Home & furniture: freight + duty amplifies ticket price; retailers shift to nearshoring or private‑label redesigns.

📊 Sector impact matrix

| Sector | Exposure to U.S. demand | Risk from 25–50% duty |

|---|---|---|

| Textiles & apparel | High for knitwear, basics, athleisure | Severe: rapid buyer substitution and margin crush |

| Gems & jewellery | High for cut & polished diamonds | Severe: promotions timed to push supplier prices down |

| Seafood | Medium‑High for shrimp & fish fillets | High: perishability + certification costs |

| Chemicals | Medium—varies by HS line | Medium‑High: intense competition from ASEAN/EU |

| Auto components | Medium via Tier‑1/Tier‑2 supply | Medium: contract clauses ease but deadlines bite |

| Electronics | Low‑Medium (exemptions matter) | Low (current): monitor policy revisions |

🧮 Landed‑cost math in plain English

| Scenario | Landed‑cost change | Likely margin outcome |

|---|---|---|

| Baseline (pre‑2025) | 0% incremental | Normal: negotiated markdowns only |

| +25% India add‑on | +18–25% after freight & vendor splits | Tight: suppliers absorb, buyers delay hikes |

| Stacked to ~50% | +40–55% depending on HS code | Critical: cancellations, re‑sourcing, SKU redesign |

🧵 Textiles & apparel — ground truth from mills to malls

India’s knitwear and woven exporters feed on the basics (tees, innerwear, athleisure) and mid‑ticket fashion where buyers value reliability over trend risk. The sharp spike in duty overnight destroys CMT economics premised on volume and consistent markdown calendars. U.S. retailers having in-house design private‑label lines are now hammering their factories force suppliers to re‑engineer skus—shorter hemlines, lighter gsm, less trims counts—to claw back cm savings without evident slippage in quality. Back home, in Tiruppur and Noida clusters, overtime freezes, yarn renegotiations, a move to open‑width processing to reduce waste: all are juggling acts. The kicker: rivals in Bangladesh and Vietnam can offer the same basics with lower duty walls, making this a buyers’ market (unless India can counter with speed, quality or design services).

💎 Gems & jewellery — substitution risks and credit stress

- 💳 Retail finance: U.S. chains use 0% APR promos to stimulate demand, then claw back margin from suppliers.

- 💧 Inventory cycles: polished stones sitting longer increase interest cost for Indian vendors; memo terms tighten.

- 🔁 Lab‑grown pivot: buyers swap some natural diamond SKUs for lab‑grown to preserve sticker prices.

- 🧾 HS code vigilance: minor misclassification at entry can add penalty risk on top of duty.

- 🤝 Consignment models: more partners shift to sale‑or‑return, moving risk upstream to India.

🦐 Seafood & agrifood — cold‑chain realities

Every added day in transit chips away at quality and increases the chances of claims for shrimp and fish exporters. Layered duties to ~50% clash with FDA testing windows, prompting buyers to trim volume or seek drastic price resets. Some U.S. importers shift to Latin American suppliers to juggle shelves for Lent and summer grilling, while Indian firms look at value‑added formats (marinated, ready‑to‑cook) that justify higher unit economics. Clusters such as those in Andhra Pradesh, Gujarat, hesitate to curtail spoilage by preventing water contamination, handling speed and in-out time reductions in packhouse, ice‑plant management and co‑loading.

🧪 Chemicals & pharma — exemptions and cracks

- 🧪 Pharma formulations & APIs: many remain exempt; vigilance is needed on input chemicals that may carry new duty.

- 🧴 Dyes/intermediates: customers in the U.S. can switch to EU or ASEAN producers; Indian firms must sell process stability and REACH‑style compliance as differentiators.

- ♻️ Specialty chemicals: sticky once qualified, but new duty can delay plant approvals and audit visits.

- 🧮 Price pass‑through: contract formulas with feedstock indices help—renegotiate to include duty escalators.

🔩 Auto components & machinery — OEM pipeline risk

Tier‑1 and Tier‑2 suppliers into Detroit and Southern U.S. plants tend to be bound by long‑horizon contracts pegged to model years. A spike in workload occurs after tooling and PPAP has been sunk, which endangers the profit bridge. A few OEMs agree to price changes if suppliers show uncontrollable cost; others ramp nearshoring to Mexico. Next, the Indian suppliers with the warehouses in the U.S. then have leverage to manage VMI and A/B testing: ship old product at old prices, make the new product into an additional sku (we will call it the duty-inclusive version). The goal should be competitive cost with the machine tools of an Traub or Nakamura, able to make the nines to maintain the high‑spec niche where switching costs are real and/or capable of turning generationally on a single insert if needed while investing in forging quality and precision machining to fight the bleeds.

📱 Electronics & IT hardware — exemptions today, watchlists tomorrow

- 📱 Smartphones and some consumer electronics currently sit in the exempt column; brands should still file ruling requests for clarity.

- 💻 IT hardware subject to separate regimes may be unaffected—until rules change. Maintain scenario boards.

- 🧭 Accessory lines (chargers, cables, cases) can be caught in HS reinterpretations; keep advance rulings handy.

- 📦 ODM partners should prepare dual‑label BOMs that enable ASEAN assembly shifts if needed.

🧭 State‑wise heatmap — clusters under pressure

- 🧵 Tamil Nadu (Tiruppur, Chennai): knitwear, leather accessories, auto components. Expect shift to quick‑response orders.

- 💎 Gujarat (Surat): diamonds; watch polishing unit cash cycles; scale up lab‑grown exposure carefully.

- 🦐 Andhra Pradesh/Odisha: seafood hubs; invest in packhouse QA and brand‑side contracts.

- 🛠️ Maharashtra (Mumbai, Pune): engineering goods and jewellery; combine VMI with design services.

- 🧪 Gujarat/MH: chemicals; lean into compliance story to justify premiums.

🚢 Compliance & customs playbook — avoid leakage

- 🧾 HTS correctness: lock classification with binding rulings; mis‑entries can add penalty on top of duty.

- 🕘 Transitional windows: document on‑board dates; some shipments loaded before the cutoff qualify for relief.

- 🧰 Drawback/Remission: maximise RoDTEP, duty drawback, and state incentives; maintain traceable BOMs.

- 💱 Hedging discipline: align forward cover with shipment dates; avoid speculative positions.

- 🧪 QC evidence: fewer rejections = fewer re‑imports; log AQL results and keep photo evidence.

🧮 Case study — a Tiruppur knitwear exporter

A knitwear house in mid‑size was hit with a surprise 25% duty add‑on for a U.S. big‑box order on 600,000 tees. The buyer requested a 9% price reduction or a SKU overhaul. The exporter developed a “lite knit” version (‑10 GSM), substituted metal trims with bartacks and normalized dye lots to minimise wastage. Savings: 5.8% of FOB. They took a broom to the duty pain 50:50 and landed a three‑month extension with an in‑season reord option based on sell-through. Power move: a video walkthrough of the factory’s needle cooling upgrade that reduced broken stitches, raising enough of the buyer’s confidence to commit volume despite duties.

🧮 Case study — a Surat diamond polisher

A polishing shop that provides mid‑range 69avigate and bridal jewellery experienced discounts planned to coincide to with introduction of the new duties. U.S. partners were driving lab‑grown SKUs and slashing consignment windows. And that the Indian vendor shifted and offered 15% capacity switched to CVD lab-grown, ESG certification to protect unknown lines, and even risk‑sharing ‑ if sell‑through was 70% by week six then buyers had a 1.5% rebate, if less, volumes switched to CVD at a previously agreed margin. Result: inventory days decreased and cash flow was steady despite unit margins contracting.

🧩 Playbook — pricing, design, currency, capacity

- 🧮 Duty‑inclusive price ladders: show buyers two ladders—value and premium—with full landed cost visibility.

- 🧵 Engineering for affordability: reduce trim complexity, consolidate colors, and adopt modular patterns.

- 💱 Rupee strategy: treat a weaker INR as a temporary buffer, not a crutch; lock benefits into contracts.

- 🧰 Capacity swaps: move commodity SKUs to lower‑duty geographies via partner networks; keep high‑spec at home.

- 📦 Near‑port warehousing: cut dwell times and capture sailing windows for any relief clauses.

🌏 Diversification corridors that actually work

1) Zhang13, 2021 3 Indian exporters can wage shave their US exposure through construction of CEPA/CETP led channels : UAE (re ‑ export hubs), EU (sustainability premium for compliant goods), UK (fashion/jewellery nitches), ASEAN (regional supply webs). The secret isn’t just market entry but repeatability — language localisation, compliant packaging and returns infrastructure. Japan and South Korea, meanwhile, reward good documentation quality and punctuality with lengthy contracts. In West Asia and Africa, there are opportunities in agri‑processing and basic apparel where Indian companies already have yarn and fabric advantages.

How India Can Diversify After Trump Tariff Shock: ASEAN, EU, and Beyond

🧠 Marketing & D2C survival — say it before the cart

- 📣 Transparent pricing: explain duty‑driven hikes; use FAQ pop‑ups and cart notes.

- 🧧 Bundles that offset sticker shock: add‑ons with high perceived value (free tailoring, extended warranty).

- 🧭 Local language ads for diaspora clusters; emphasise origin, craft, and fair trade.

- 🧪 Try‑before‑buy for jewellery and apparel in U.S. metros; reduces returns, protects margins.

🧑⚖️ Policy and legal levers exporters can use

India’s bouquet of policies—RoDTEP, RoSCTL for apparel, state electricity subsidies, PLI for components—can mitigate the impact. Export councils need to agitate for priority export credit, faster input‑GST refunds and testing lab capacity to reduce holds. At the bargaining table, buyers can obtain duty‑sharing addendums if provided with smoking gun files (duty notifications, HTS rulings, and BOMs). At home, expedited port EDI and road freight facilitation reduce non‑tariff frictions of the kind the exporters can control.

📈 Market & investor lens — rupee, equities, credit

A higher effective duty wall, reduces order visibility and increases working‑capital cycles for the listed exporters Sucharit Iyer, Joint Managing Director at Bonito fabrics.exporters. When it comes to equity in the markets sell first and model later: rupee weakness can act as a partial offset to FOB pain but is a signal of imported inflation back home. Look for bank commentary on MSME stress and NPA slippage in export-heavy states, as well as CP/CD spreads for mid-cap names that rely on U.S. retail. Defensive plays are IT services (dollar revenue, low tariff exposure) and pharma (exempt lanes). According to studies, the higher annual cost for American households of the 2025 wave would create pressure that could eventually nudge retailers to accept selective price increases.

Market Fallout: Trump’s Tariffs Send Rupee Weak, Shake Investor Sentiment

🧰 CFO/export team checklists that save weeks

- 🧾 Re‑quote library: standard templates with duty lines, freight, and incoterms.

- 🧪 HS audit every SKU; seek binding rulings where ambiguous.

- 📦 Customer tiers: A/B your top accounts—who can absorb hikes vs who needs redesign.

- 💳 Trade credit: diversify insurers; negotiate pay‑later on inputs.

- 💱 FX rules: auto‑hedge on booking; review stop‑loss bands weekly.

- 🧰 Data room: keep certifications, test reports, and prior CBP entries ready for spot checks.

🧭 For workers & MSMEs — cushioning the blow

- 🧑🏭 Shift scheduling to preserve jobs: four‑day shifts with training on the fifth day.

- 🎓 Skill refresh: QC, CAD markers, and compliance logs—raise value per worker.

- 🧺 Local procurement: reduce input imports to defend cash cycles.

- 🤝 Cluster cooperation: shared freight contracts, pooled testing slots, and buyer roadshows.

- 🧾 Government touchpoints: district industry centres for quick credit and utility relief.

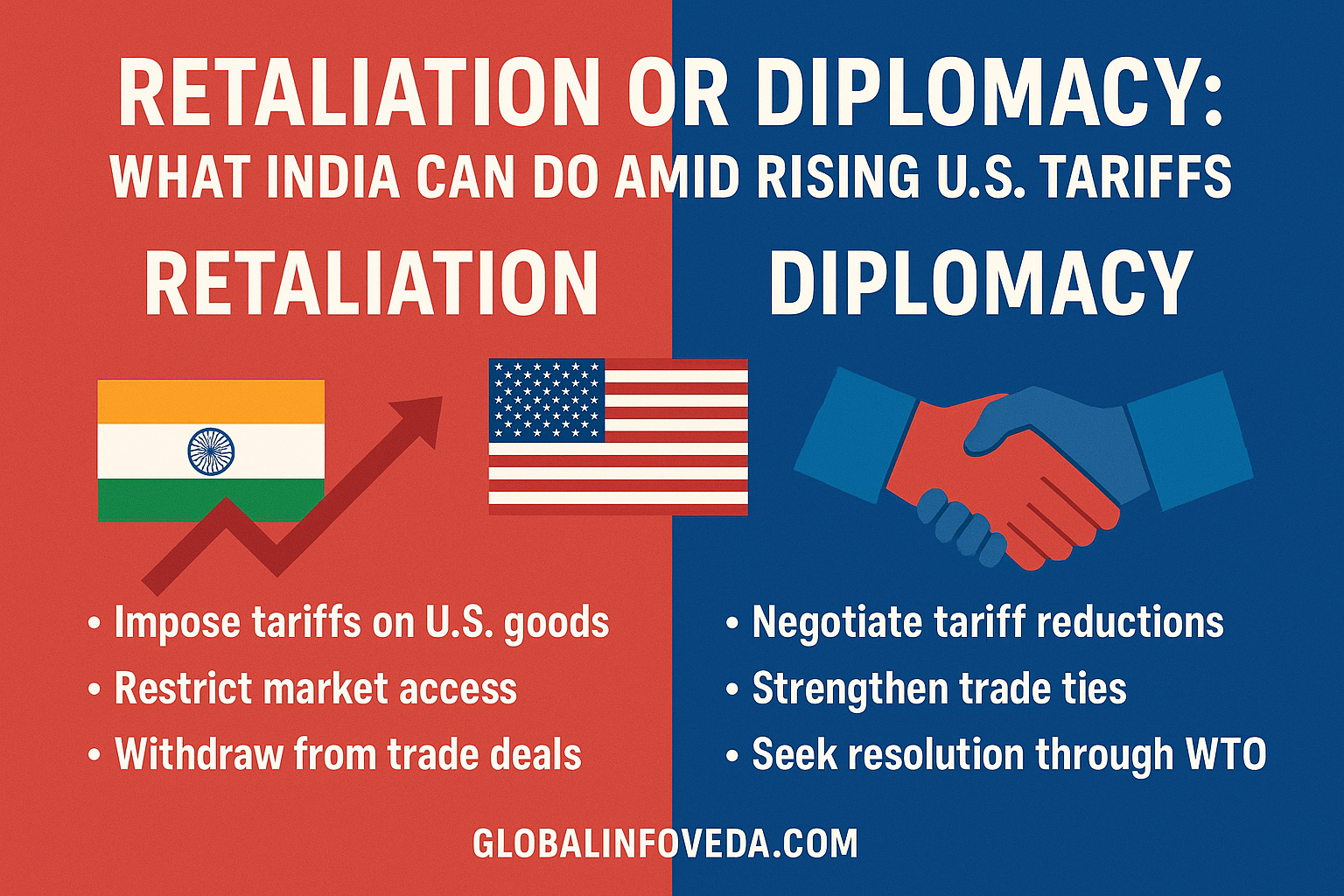

Retaliation or Diplomacy: What India Can Do Amid Rising U.S. Tariffs

🇺🇸 What American households and retailers face

A tiered system of tariffs lifts U.S. shelf prices over time, though buyers can buy themselves some time by pushing down supplier margins. Retailers will re‑source or redesign SKUs where tariffs are at ~50%, and for essentials, consumers face smaller packs, cheaper materials, or fewer features. Independent studies have estimated that the net cost to the average household of the 2025 wave of tariffs would reach several thousand dollars annually, with lower‑income households paying a higher share of the inflation pain. Those dynamics can loop back to India — if U.S. demand cools, volumes can fall even without an additional tariff.

U.S. Families Could Pay $3,800 More a Year Due to Tariffs

🧠 FAQs

- Is the duty universally 25%? No. The U.S. announced an additional 25% for India, layered over prior duties; many HS lines effectively face ~50%. Exemptions apply to select smartphones and pharma.

- Can exporters split the pain with buyers? Yes—through duty‑sharing clauses, redesigned SKUs, and promotional calendars that smooth price jumps.

- Will a weaker rupee solve it? It helps FOB competitiveness but can’t erase a 50% wall; use gains to upgrade and de‑risk.

- What about retaliation? India can calibrate WTO‑consistent responses, seek bilateral tracks, and expand non‑U.S. markets.

- How long will it last? Treat 2025–2026 as a planning horizon; policy can shift, but resilience plans should not wait.

🧠 Demand elasticity checkpoints by sector

- 🧵 Basics vs fashion: staple tees and innerwear show higher price elasticity—small hikes move demand; premium fashion absorbs design‑led upgrades better. Map each SKU to an elasticity band before you quote.

- 💎 Natural vs lab‑grown: diamonds split into two demand curves. Lab‑grown is price‑led; natural is scarcity‑narrative‑led. Keep calendars distinct so promotions don’t cannibalise margins.

- 🦐 Commodity vs value‑added: plain shrimp is hyper‑elastic; marinated or ready‑to‑cook formats earn feature credit. Push value‑add before price talk.

- 🧪 Bulk vs specialty: basic dyes and solvents face immediate substitution; specialty chem with qualification friction is stickier—defend documentation.

- ⚙️ Aftermarket vs OEM: auto components sold into aftermarket move faster on price; OEM volumes move slower but are binary at model changeovers.

- 🛋️ Flat‑pack vs finished: knock‑down furniture can shift origin by component; fully finished faces re‑sourcing friction—use that window to renegotiate.

🧮 Worked examples — cost bridges on real SKUs

Think of a $2.10 FOB cotton tee en route to a U.S. discount store. So, pre‑2025, it was $3.10c land of a land. A +25% India duty should take land to $3.80, and stacked 50% would take ~$4.60. That still leaves $1.39 for retail margin and markdowns — not enough if the retailer caps shelf at $5.99. The fix is multi‑pronged: shave 5–7% via new fabric and trim engineering (‑10 GSM, simplified neckline), shift packing to bulk poly with size stickers, and co‑fund a limited‑time promo to test demand elasticity. Evidence‑based small changes can save the plan without diminishing the view of the brand.

Now they’re a $450 bridal ring (real diamond) on keystone pricing. A stacked ~50% duty either drives a purchase of a lab‑grown for the same price or a value story—ESG certification, superior cut, made‑to‑order craftsmanship—needed to earn a place on a higher shelf. Sellers that offer sell‑through dashboards (unit turns, returns rates) are the ones that keep doors open while the others get cut.”

For Tier‑2 auto parts — something like a forged knuckle at $17 FOB — the tooling is sunk, and the PPAP process is complete. A 25% added duty can be spanned with a temporary price‑recovery clause plus VMI near U.S. plants to eliminate logistics waste. Over 2–3 quarters suggest a material‑agnostic redesign that shaves minutes of machining while maintaining safety specs.

🛠️ HS‑code guardrails and re‑engineering map

- 🧾 Binding rulings: secure CBP letters for ambiguous SKUs; align HS codes across invoice, packing, and label.

- 🧪 Bill of materials clarity: list fiber % and finishes; surface treatments can shift HS lines.

- 🧵 Garment tweaks: pocket count, closure type, and lining can alter classification—design with codes in mind.

- 🧴 Chemicals: exact CAS and concentration prevent misclassification; add SDS with translations.

- 🧰 Assemblies: consider shipping sub‑assemblies for local completion where rules allow, without violating origin.

📊 Policy paths 2025–2026 — what to plan for

| Scenario | Likelihood (next 12–18m) | Exporter response |

|---|---|---|

| Duties hold | Base case | Lock duty‑sharing clauses; accelerate diversification |

| Selective relief | Moderate | Prepare evidence files to qualify cargo; reload cancelled POs |

| Further escalation | Tail risk | Trigger ASEAN assembly options; protect cash and credit lines |

🧰 Financing the shock — instruments and cadence

The duty wall stretches working capital and challenges discipline. Opt mty to neutralise cash cycle; combine with bill discounting (backed by buyer’s creditworthiness). ECB windows can capex QA labs and energy efficiency so you keep price down with performance. Condition supplier credit on measured efficiency improvements (reduction in waste, energy savings), not on vague assurances. For MSMEs, district credit facilitation plus credit guarantee schemes can fill payroll and avoid shedding skilled labor.

🚚 Logistics pivots that pay back

- 🚢 Sailing window mastery: near‑port consolidation and VGM compliance stop rollovers that kill promotions.

- 📦 Carton‑to‑shelf designs: reduce DC touchpoints; buyers trade duty pain for low handling.

- 🧭 Alternate ports: test Mundra/Ennore vs your default; dwell time variance matters.

- 🧊 Cold‑chain telemetry: shrimp/fish with live temp logs earn fewer claims and better renegotiation odds.

- 🏷️ UPC continuity: preserve barcodes when redesigning SKUs so shelves don’t need resets.

🏷️ Contract levers worth the ink

- 🧠 Material variance clauses tied to indices and duty escalators.

- 💳 Payment schedules that release when CBP clears entries.

- 🧾 Defect thresholds with independent AQL audits to reduce dispute time.

- 🔁 Right‑to‑rework in destination markets for apparel trims and packaging.

- 🧰 Data‑sharing: weekly POS and return feeds unlock smarter replenishment under tariff constraints.

🧪 Metrics dashboard for the next 90 days

Track fill rates, chargebacks, claim percentage, order-to-cash days, FX realisation and SKU survival (what stayed in plan post duty). For clothing, track returns by size—mis‑graded fit is profit bleed. For jewellery, log prove-up rates (earring/ring with prove-up) and repair tickets. For seafood, limit temperature excursions time out to claims and then renegotiate carriers. Print a weekly, one‑page sheet to synchronize production, finance and sales.

🧭 People and culture — holding teams together

Tariff seasons can sour morale. Cycle teams through buyer calls so engineers can hear commercial truths; reward waste‑cut ideas with headline credit; and invest in safety and skill so the shop floor feels progress. Talk in basic figures — duty impact per piece, minutes saved per style — so everyone understands his importance to survival.

🧩 State‑to‑sector play ideas

- 🧵 Tiruppur: shared effluent and heat‑recovery upgrades cut utility costs and score sustainability points.

- 💎 Surat: carve out a pure CVD line with clear origin marking; keep natural and lab‑grown workflows separate.

- 🦐 Andhra coast: co‑op ice plants and QC labs; brand traceable aquaculture with QR farm logs.

- 🛠️ Pune/Nashik: consortium buys for tool steel and cutters; common CMM labs for faster PPAP.

- 🧪 Dahej/Vapi: pooled haz‑waste handling; faster audit slots win specialty orders.

📈 What buyers are telling their boards

U.S. retailers say they will defend value price points with pack‑downs, feature trims, and origin shifts before taking sticker hikes. They also like exclusive capsules that justify a premium narrative without heavy promo. Suppliers who bring ready creative (tags, signage, product stories) get a longer leash while finance teams reassess.

🧭 Contingency calendar — 12‑month rhythm

- 🗓️ Q1: lock duty‑sharing addendums; file binding rulings for grey HS lines; freeze yarn/metal buys for 90 days; stand up a one‑page buyer dashboard (OTIF, AQL, claim %, POS turns).

- 🗓️ Q2: pilot ASEAN assembly on 1–2 SKUs where math works; shift to near‑port consolidation; co‑fund one promo to test elasticity; train teams on evidence‑pack hygiene.

- 🗓️ Q3: scale winning SKU variants; expand VMI or U.S. warehousing for components; reset price ladders for holiday; prune SKUs that only worked pre‑duty.

- 🗓️ Q4: deepen non‑U.S. corridors (EU/UK/West Asia); codify learnings into SOPs; plan FY cash cycles around refunds/drawback cadence.

🔧 Execution levers that move the needle

- 🧾 HTS certainty + evidence packs: rulings, BL dates, AQL logs, photos—reduce port friction and speed duty‑sharing sign‑offs.

- 🧵 Duty‑smart SKU redesign: trim GSM/trim counts, consolidate colorways; split value/premium ladders with transparent landed math.

- 🚢 Near‑port + sailing discipline: fixed sailing windows, carton‑to‑shelf packaging, and alternate ports to cut dwell time.

- 💳 Finance cadence: PCFC + invoice discounting; weekly sweep of RoDTEP/drawback/GST; align FX covers to shipment gates.

- 👥 People & cluster cooperation: pooled testing slots, shared freight, short up‑skilling sprints (AQL, CAD markers, digital QC).

📊 At‑a‑glance KPIs for a weekly dashboard

- 📦 Fill rate and chargebacks/1k units by account.

- 🧪 AQL fail % and top‑3 defect causes (heatmap).

- 💱 FX realisation vs booked cover, with stop‑loss notes.

- 🧾 Order‑to‑cash days and claim %; reopeners won/lost.

- 🛒 POS sell‑through and returns (size curve, shade variance).

📚 Sources

- The White House — Executive actions on reciprocal tariffs & India‑specific duties: https://www.whitehouse.gov/presidential-actions/2025/07/further-modifying-the-reciprocal-tariff-rates/ and https://www.whitehouse.gov/fact-sheets/2025/08/fact-sheet-president-donald-j-trump-addresses-threats-to-the-united-states-by-the-government-of-the-russian-federation/

- Congressional Budget Office — Tariff revenue and household impact updates (2025): https://www.cbo.gov/publication/61697

- Reuters — Coverage of U.S. tariff escalation on Indian goods and sectoral exemptions (Aug 2025): https://www.reuters.com/world/india/indian-textiles-jewellery-slapped-with-50-trump-tariff-pharma-phones-exempt-2025-08-08/ and https://www.reuters.com/world/india/india-hit-by-us-doubling-tariffs-plans-cushion-blow-2025-08-27/

- Press Information Bureau (Government of India) — Ministry of Steel note on U.S. tariff impacts: https://pib.gov.in/PressReleaseIframePage.aspx?PRID=2110254

🧠 Final insights

The 25% India tariff — and its ~50% stacked effect on a large number of India export sectors — isn’t a line-item hike, it’s a regime shift in price, risk, and relationships, across the India–U. S. corridor. Winners will map HTS certainty, co‑design duty‑smart SKUs, lock FX discipline, and open new corridors while protecting their home clusters with training and shared services. There’s a lot that policymakers can do to speed up refund cycles, expand testing capacity and simplify logistics. With more control over what exporters can and should do, they may find it easier to negotiate what they can’t or shouldn’t do. There will be an added cost for consumers in America, a cost not just shifted but very much cumulative; retailers will manage pack‑downs and re‑sourcing; and India, with focus and coordination, has the ability to migrate volumes to the geographies where quality + reliability still commands a premium.

👉 Explore more insights at GlobalInfoVeda.com

{kind=link}