💳 Introduction

Credit bureaus in India are quietly and significantly being updated in 2025 as rent payments and UPI activity shift from the periphery to influence the credit bureau conversation. For millions of urban renters and digital‑first workers who do pay perfectly every month but don’t have traditional credit lines, it could mean the difference between a thin file and a healthy credit profile. That’s far more than loan access at play — it’s fairer pricing, quicker approvals and opportunity for households that live cash‑flow clean but leave no formal trail. This deep dive explains the changing RBI and CIC landscape, what landlords and prop‑tech apps can report on‑time rent, what constitutes consented UPI signals, how lenders might use them and what guardrails they’ll have to respect in terms of privacy under India’s new data protection regime. For that we’ll map practical playbooks for tenants, fintechs, NBFCs and banks with India‑specific context, comparisons and real stories.

Meta description: India 2025: credit scores begin to weigh rent and UPI data. See how norms are changing, what counts as consent, benefits, risks, FAQs, and future outlook.

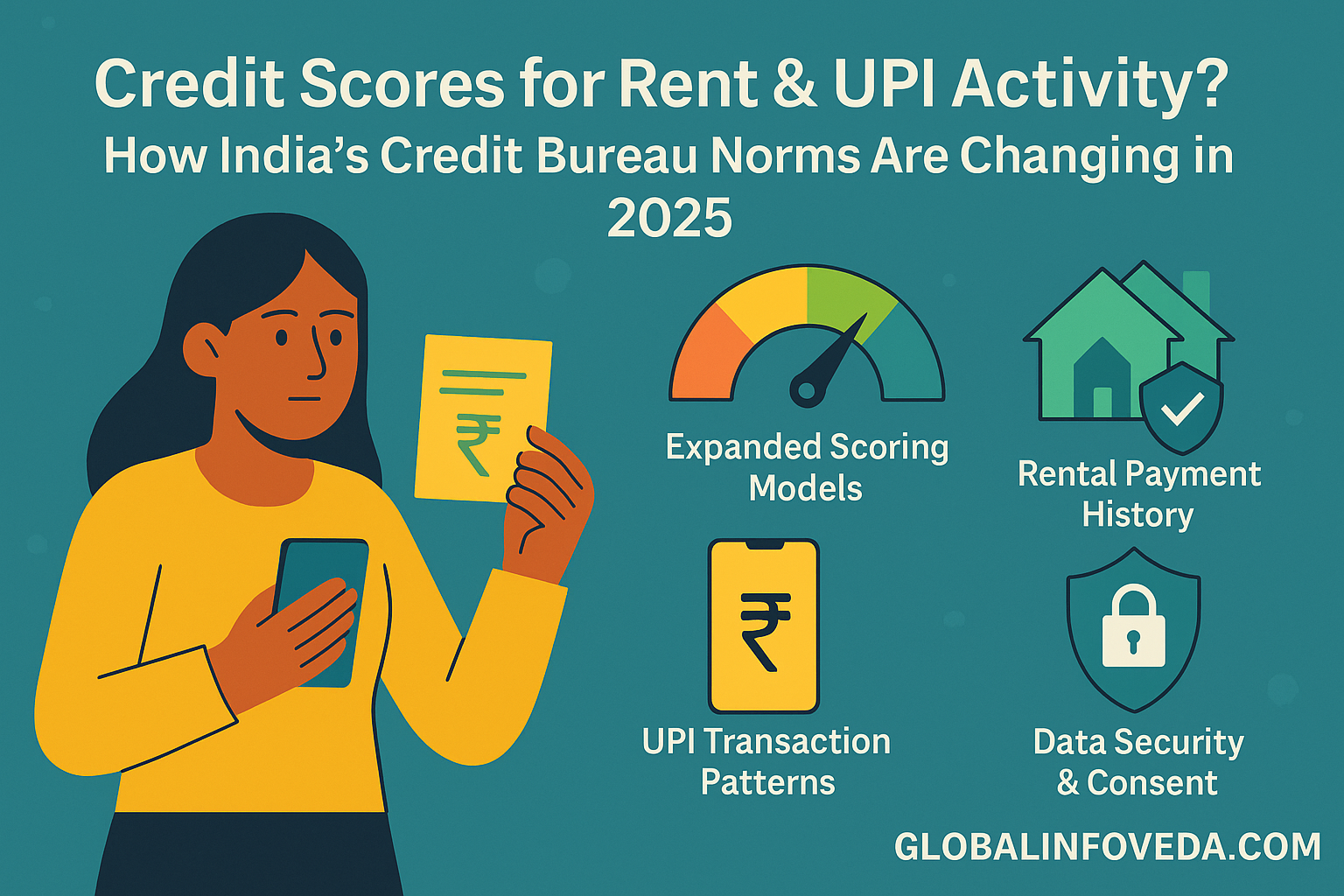

🧭 What’s changing in India’s credit data universe

Until now, India’s credit bureaus—TransUnion CIBIL, Experian, CRIF High Mark and Equifax—were dependent on repayment track records of loans and cards that were shared by banks and NBFCs. That left a vast “thin file” population: renters who had good UPI, rent discipline and no formal credit lines. In 2025, policy momentum on open finance, consent‑based data sharing, and financial inclusion is prodding bureaus and lenders to be more open to alternative data—with two leading candidates: on‑time rent and selected, aggregated UPI signals. The logic is simple: if someone has paid ₹18,000 every month for 24 months, without a miss and regularly clears UPI dues, that is solid evidence of repayment capacity and financial hygiene.

🏠 Where rent fits into credit scores

In global markets, reporting of rent has assisted renters in understanding how they can create or strengthen their credit without first borrowing. India is playing catch-up through prop‑tech rails, housing app integrations, and landlord portals that validate rent receipts, bank credits, and lease metadata. The idea is not to hit negative late rent hard, but to document positive payment history to the extent you can. Anticipate lenders considering 12–24 months of on‑time rent a strong stability indicator for entry‑level products (two‑wheeler loans, secured cards and small personal lines). How each credit bureau will weigh rent will vary, but the trend is clear: timely rent is a proxy for reliable cash flow.

Housing Finance on Trial: NHB Tightens Rules on High‑Value Loans

📲 Where UPI activity may matter—and where it won’t

UPI is India’s answer to how to pay friends, shops, cabs and bills. But not every UPI data point is relevant to a credit score. In a consented world, what matter for this are repeat signaling obligations (utility, rent via UPI), consistency of bill‑pay, basic cash‑flow regularity — not who you tipped last night. You can expect the models to like binary and aggregate features (e.g., “on‑time bill streak present: yes/no,” “volatility in range”) more than any kind of granular, personally sensitive detail. And as for those cases in which it may not be clear whether a payment product is able to use UPI, banks should down‑weight UPI attributes to prevent bias and privacy creep, and in turn use the attributes as eligibility and pricing support for thin files, but not as hard negatives.

UPI 3.0 Introduces Voice Payments: A Leap Toward Conversational Transactions

⚖️ Old playbook vs new rails (quick view)

| Lens | Earlier approach | 2025 approach |

|---|---|---|

| Data sources | Loans, cards, overdrafts | Loans + rent + consented UPI aggregates |

| Inclusion | Favors existing borrowers | Helps thin‑file renters and gig workers |

| Consent model | Implicit via lender furnishing | Explicit, granular, revocable via Account Aggregator/app flows |

🧩 The consent stack: how data should legally flow

Consent‑based sharing is now at the heart of India’s data rails. The AA framework enables sharing of financial information between regulated entities in a consented manner, using standard digitally signed consent artifacts. For rentals, the streams may include bank statements, verified rent receipts and escrow or rent‑collection apps. For UPI what is reasonable is aggregate (signals from use of PSP apps or bank statements (such as ‘recurring payment’ flags) not itemised listing of social spending. And it all must be purpose‑limited, time‑bound and revocable. Lenders should keep only what is necessary for decisioning and audits; anything beyond that invites regulatory and reputational risk.

🛡️ Guardrails under India’s policy regime

What are the three anchors for rent and UPI flowing into credit scores? (OUP) T he three anchors are related to (1) RBI’s prudential and consumer‑protection direction, (2) CIC rules under CICRA 2005, and (3) the DPDP Act, 2023 (guiding consent, minimisation of copying, and breach accountability). In practice, that’s no approval of “dark patterns;” clear opt-in; consent audit trails; and a robust dispute mechanism so that renters can contest m is‑reporting.” It also requires that lenders demonstrate how the use of alternative data impacts pricing and exclude attributes that self-serve as a proxy for a protected class.

The Rise of Open Finance: From Banking to Full Financial Ecosystems

🧠 How models might actually use rent and UPI

Prediction stability and generalization are the bread and butter of scoring systems. Rent has regular, binary, and very interpretable features: on‑time vs not, amount vs income, streak length. We provide a cadence and regularity‑related predictor measured (e.g., whether any of the auto‑pay and the number of bill categories paid without any bounce), and Varying month to month within a band:week We provide a band in which 1 more is paid, lesser as many, number of bounce, whether there is no shopping/browsing, and whether the subscriber has an account with another operator or not. Thin‑file scores can be expected to consist of traditional tradelines (if present) plus 3–5 coarse rent/UPI features, while applicants in the full‑file group may observe modest motion. It is important to note that the adverse action rationale never should reference UPI merchant types or personal relationships, only high‑level payment reliability indicators based on consumer‑approved information.

📊 Inclusion trade‑offs (consumer view)

| Theme | Potential upside | What to watch |

|---|---|---|

| Access | Credit score lift for renters, faster approvals | Data accuracy, dispute resolution speed |

| Pricing | Lower interest for consistent payers | Over‑fitting to short streaks |

| Privacy | Consent and revocation via AA | Scope creep beyond purpose |

🧮 A worked example: renter with a thin file

Say hello to Anita, 27, with no credit card and one education loan closed two years ago, one of very short tenure. She makes payments of ₹19,500 as rent every month using UPI. By tapping into a rent‑collection app married with an AA flow, she agrees to share 12 months of validated rent receipts and a binary flag indicating if she paid UPI bills on time. One such thin‑file hole gets plugged by a “capacity & discipline” feature, and suddenly her credit score is 25–40 points higher. With that boost she then can qualify for a secured card that later graduates to unsecured as the girl’s tradeline ages. If her landlord doesn’t report promptly, she can dispute it with documentation to the bureau.

📚 Lender view: where the rubber meets the road

Banks and NBFCs crave explainability. Rent is so darned clever because it’s human‑readable: “paid ₹X on Y date each month for N months.” UPI is a bit trickier; it’s safest to use binary adherence signals (auto‑pay for essentials, no penal flags) rather than category‑level details. Lenders may also originate with policy overlays: rent supporting entry‑level products or UPI stability driving pricing or credit‑limit decisions for small lines. For high‑ticket loans these are extras, not deal‑breakers.

🧷 Tenant playbook: getting credit for the rent you already pay

- 🟢 Use verifiable rails. Pay via bank transfer/UPI with clear narration (e.g., “Rent‑July‑Flat 504”). Avoid cash.

- 🧾 Collect documents. Keep lease, owner PAN, rent receipts, and bank proofs in a single folder.

- 🏦 Opt‑in to reporting. If your prop‑tech or landlord offers bureau reporting, consent after reading what is shared and with whom.

- ⏱️ Streak discipline. Set a standing instruction a few days before due date; document any landlord delays.

- 🧑⚖️ Dispute promptly. If a late mark appears in error, use the credit bureau dispute portal with receipts.

🧱 Landlord & prop‑tech playbook: report responsibly

- 🧩 Verify identity. KYC for tenant and owner to reduce false positives.

- 🧮 Automate reconciliation. Map UPI/IMPS credits to tenant IDs; minimise manual handling.

- 📝 Clear consent UI. Plain‑language screens explaining what is sent to which credit bureau and why.

- 🔐 Data minimisation. Send on‑time/late flags, amounts, and dates; avoid unnecessary metadata.

- 🧯 Fair treatment. Give tenants grace for bank outages; publish a dispute email and turnaround SLAs.

🏦 Fintech & bank playbook: design for inclusion, not creep

- ✳️ Feature choice. Prefer rent streak and bill‑pay streak indicators over granular merchant‑level UPI categorisation.

- 🧪 Champion‑challenger. Run rent/UPI features in shadow models before full adoption; monitor for bias drift.

- 🧭 Adverse action clarity. If declined, cite understandable reasons (e.g., insufficient history) rather than opaque UPI labels.

- 🔍 Auditability. Keep an evidence trail of consent, data versions, and feature derivations for regulators.

- 🧰 Exit ramps. Make revocation easy; purge derived features if consent is withdrawn and not legally required to retain.

🧠 India‑specific nuances that move the needle

India’s rental market ranges from formal lease agreements in metros to verbal understandings in small towns. Digitisation is uneven: some states have e‑stamping and online rent receipt tools, others rely on manual slips. UPI adoption is near‑universal, but PSP app features vary in bill‑pay reliability. Monsoon and festival cycles affect cash flow; so do bonus seasons. Lenders should normalise seasonality and avoid penalising cultural patterns. Finally, remember women often pay from joint or family accounts; models must not misread shared inflows as risk.

🔒 Privacy, DPDP Act, and consumer rights

Under the DPDP Act, 2023, processing of personal data requires consent, and users have rights to access, correction, and erasure (with lawful exceptions). Any use of UPI aggregates or rent records for scoring must be purpose‑limited to credit decisioning, kept secure, and deleted or anonymised when no longer necessary. Dark‑pattern nudges (“continue to see score”) are out. Clear consent dashboards and AA artefacts are in. Consumers should be able to see when their data was pulled, by whom, and for what.

📊 Which data should count, and how (design rubric)

| Design choice | Safer implementation | Risky implementation |

|---|---|---|

| Rent | Verified on‑time streak + amount + lease metadata | Free‑text claims without proofs |

| UPI | Aggregated flags (auto‑pay present, bill categories active) | Merchant‑level categorisation of personal spend |

| Consent | Time‑bound, revocable via AA | One‑time blanket approvals with no exit |

🧪 Case study: gig‑economy worker in Jaipur

Rahul, 32, works for several platforms and pays ₹9,800 rent. His bank account has irregular inflows, but he has a perfect UPI bill‑pay streak for electricity, mobile and rent collection. With ops AA’s consent, a lender swallows up 6 months of rent streak + only a single binary “auto‑pay active: yes.” Rahul has a thin but stable credit score when he’s presented with a small BNPL line for tyres that are priced better than previously. His limit upgrades after he’s paid on‑time for nine months. When one platform paused incentives for two months, his rent streak… kept on anticipating over there.

🧪 Case study: working couple in Pune

Sana and Imran are co‑tenants in a 2BHK and divide ₹26,000 through upi. Their landlord opts for a prop‑tech portal that, with documentation, reports to just one of the credit bureaus. Either had worked little and had no cards. Twelve more months of paying rent on time + no bounces on auto‑pay utilities, and their scores cross the typical 720 threshold, for a low‑fee secured card that, in a few years, graduates. The key was verifiable rent; their food-delivery spends never went into the model.

Banking Stability or Risk? Growing NPAs Demand Swift Action

🧭 Product patterns that keep the system fair

A fair-minded lender views the rent and UPI as corroboration, not moral indictment. That includes broader acceptance for starter products and soft positives for rent streaks, and warnings about the use of merchant or social signals. It also means making positive stepping‑stones attractive: refundable deposits, upgrade paths and fee waivers in return for on‑time behaviour. Platforms need to be sharing model cards in more plain language: which features help, which obscure, and what users can do to improve the latter. And they should agree to sunset any feature that is found to have a correlation to protected traits.

🧠 Pricing, limits, and risk: what to expect in practice

Look for thin‑file applicants with rent streaks to experience slight APR improvements and quicker turnaround times. UPI aggregates might aid in sizing credit limits for small lines where traditional income proofs are noisy. But for jumbo loans, cash‑flow underwriting and documented income is still king. If your rent is in cash, you should do the next best thing: switch to UPI/bank rails with evidence. If you’re a landlord, consider holding off on reporting individual payment delays stemming from banking outages: fair play and you won’t wind up with high turnover in tenants.

🧩 State capacity and grievance redress

As alternative data grows, so must redress volume. The credit bureaus should consider manning India‑language helplines, and should set TATs for resolution of rent disputes. Why banks/NBFCs need to promote adverse action reasons that we can relate to. Prop-techs should have ombuds processes and publish quarterly accuracy stats. No trust killer is quicker than a bad LLM (wrong late mark that takes months to correct). The north star is straightforward: When a consumer can demonstrate through on‑time rent that they can afford to live in a neighborhood, the system should self‑correct.

🧰 Practical improvements you can make this month (consumer)

- ✅ Move to traceable rails. Pay rent and essentials via UPI/bank with clear narration.

- 🗂️ Centralise proofs. Keep e‑lease, rent receipts, PAN of owner, and bank screenshots handy.

- ⏰ Automate. Use auto‑pay where safe; set reminders for due dates.

- 🧭 Check your score. Review your credit score from time to time; dispute inaccuracies early.

- 🛡️ Consent hygiene. Use AA only with trusted lenders; revoke old approvals you no longer need.

🧰 Practical improvements this quarter (landlord/prop‑tech)

- 🧮 Standardise data. Adopt a unified rent receipt schema (date, amount, tenant ID, lease ID).

- 🔐 Secure stores. Encrypt at rest; restrict access to need‑to‑know.

- 🧾 Transparent flows. Share a one‑pager showing exactly which fields go to which credit bureau.

- 🧑💻 APIs over spreadsheets. Use API‑driven reporting to cut manual mistakes.

- 🧯 Grace logic. Build outage calendars and public holiday grace into your late flags.

📊 Access models: how consumers might get value

| Model | What it offers | What to verify |

|---|---|---|

| Rent reporting via app | Adds on‑time streaks to bureau file | Fees, opt‑out path, error correction TAT |

| UPI aggregate via AA | Confirms auto‑pay and bill reliability | Scope of fields, retention period |

| Starter secured card | Builds tradeline toward unsecured | Upgrade policy, deposit terms |

🧠 How this ties into CBDC and future rails

India is piloting the Digital Rupee (CBDC) with growing transaction counts. While CBDC is not UPI, both can coexist with shared consent norms and clear audit trails. Over time, CBDC receipts could provide yet another stable, low‑fraud evidence of payment discipline, especially for rent that passes through compliant wallets. Any such usage would still require explicit consent and strong minimisation.

Digital Rupee Crosses ₹300 Cr in Use: What’s Next for CBDC in India?

🧠 My take: the promise and the pitfalls

Used well, rent and UPI can improve credit scores for millions who do everything right but remain invisible to the system. The promise is fairness: price on proven discipline, not on paperwork privilege. The risk is scope creep—turning intimate payment trails into profiling. The fix is design: aggregated, binary features; opt‑in rails; robust disputes; and routine bias testing. If India gets this right, the world will study our model.

❓ FAQs

- 💡 Will paying rent by cash help my score? No. Shift to UPI/bank so there’s a verifiable trail.

- 💡 Can my landlord hurt my score unfairly? You can raise a dispute with the credit bureau and provide receipts; platforms should log landlord SLA and accuracy.

- 💡 Is all UPI data fair game? No. Only consented, aggregate indicators relevant to credit should be used.

- 💡 How long until I see changes? Many lenders look for 6–12 months of streaks before pricing moves.

- 💡 What if I revoke consent? Lenders must stop fresh pulls; retention of past data follows regulatory retention and audit needs.

🧠 Outlook: 2025–2028

Expect a careful, phased adoption. Lesser value entry‑level products — in hand‑set finance, two‑wheelers, small personal lines — will rest first on rent and later UPI. Public‑sector banks will move more slowly than NBFCs and fintechs, but once national players publish measures of success, adoption will expand. Globally, India’s AA will be referred to as a proof for consent‑based scoring on the UPI stack. Look for state portals that standardise e‑lease flows, and cities that incentivise documented rent for tenancy and credit inclusion.

GST Overhaul: How Modi’s $20B Bet on Consumption Drives Tax Reform

📚 Sources

- Reserve Bank of India (RBI) — regulations for credit information companies, consumer rights, and consent norms: https://www.rbi.org.in

- National Payments Corporation of India (NPCI) — UPI guidelines, PSP circulars, and product updates: https://www.npci.org.in

- Ministry of Electronics & IT (MeitY) — Digital Personal Data Protection Act, 2023 overview and FAQs: https://www.meity.gov.in

- TransUnion CIBIL — consumer education on credit score and dispute mechanisms: https://www.cibil.com

🧠 Final insights

Rent and UPI into Credit Scores: India’s Next Leap in Financial Inclusion—but only if consent‑first design, clear disputes, and privacy ‑respecting, discipline ‑rewarding features are factors. If you’re a renter, or like so many of us, a gig worker, your best bet is to make some verifiable streaks on some rails you already frequent. If you’re a lender or platform, you can choose to prioritize explainability, lessen your data appetite and release model cards so that your users can help you improve. A more equitable system prices behavior, not privilege — and that’s a win for both households and healthy credit markets.

👉 Explore more insights at GlobalInfoVeda.com